When it comes to choosing a mortgage, one of the key decisions you’ll need to make is whether to opt for a fixed-rate or an adjustable-rate mortgage (ARM). Each option has its own set of pros and cons, and understanding them can help you make an informed decision that aligns with your financial goals.

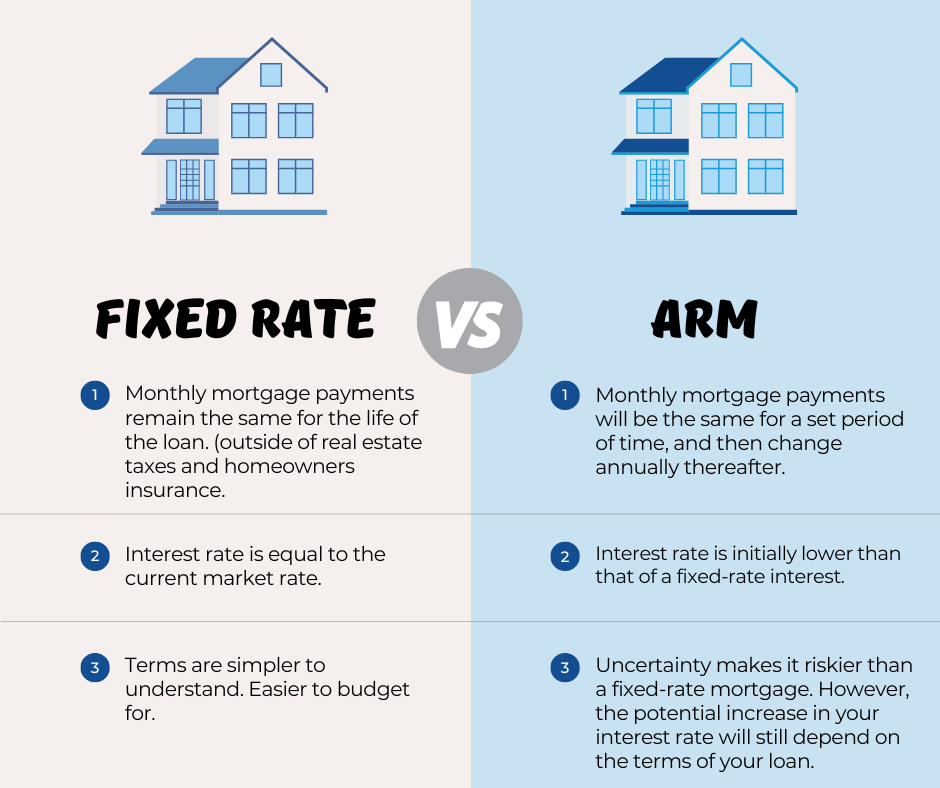

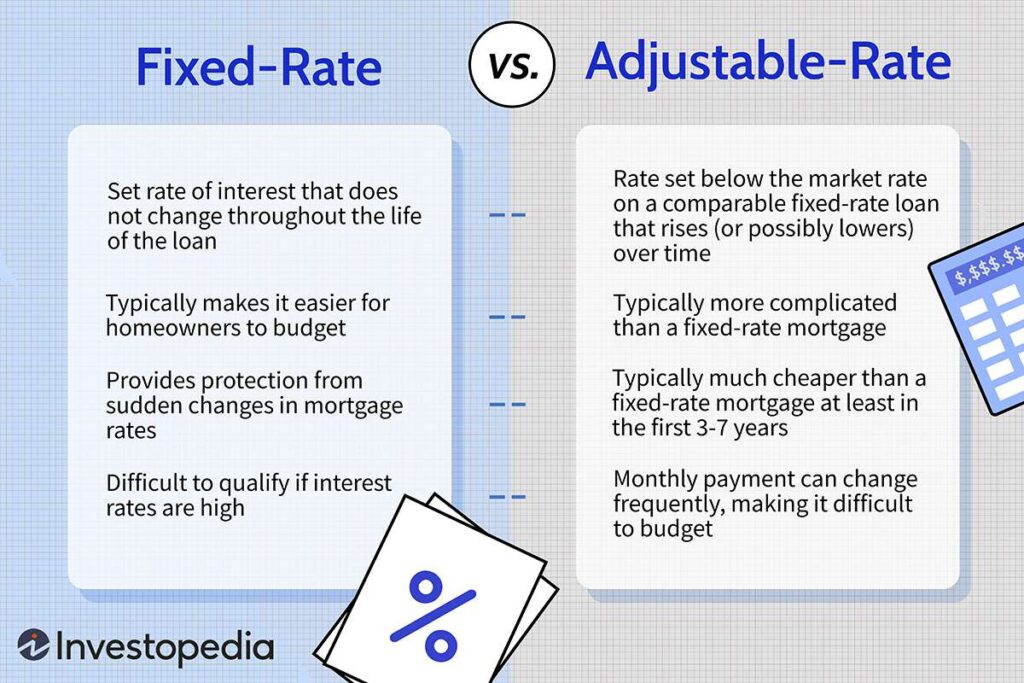

Fixed-Rate Mortgages: A fixed-rate mortgage offers stability and predictability. With this type of mortgage, your interest rate remains the same throughout the entire loan term, whether it’s 15, 20, or 30 years. This means your monthly payments remain consistent, making it easier to budget and plan for the long term. Additionally, if interest rates in the market rise, your fixed-rate mortgage won’t be affected, providing you with peace of mind.

Pros: 1. Predictable payments: Your monthly payments remain unchanged, making budgeting easier. 2. Protection against rising interest rates: Your interest rate is locked in, shielding you from potential increases in the market. 3. Long-term stability: If you plan to stay in your home for an extended period, a fixed-rate mortgage offers stability and financial security.

Cons: 1. Higher initial rates: Fixed-rate mortgages tend to have slightly higher interest rates compared to adjustable-rate mortgages. 2. Limited flexibility: Once you lock in your interest rate, you won’t be able to take advantage of lower rates in the market unless you refinance.

Adjustable-Rate Mortgages (ARMs): An adjustable-rate mortgage, as the name suggests, features an interest rate that can fluctuate over time. Typically, ARMs offer a lower initial rate compared to fixed-rate mortgages, making them an attractive option for borrowers looking for lower initial payments. However, it’s important to consider the potential risks associated with adjustable-rate mortgages.

Pros: 1. Lower initial rates: ARMs often have lower interest rates at the beginning of the loan term, allowing for lower initial monthly payments. 2. Potential for savings: If interest rates decrease in the market, your adjustable-rate mortgage can adjust downward, potentially resulting in lower monthly payments. 3. Flexibility: Depending on the terms of your ARM, you may have the opportunity to refinance or sell your home before the interest rate adjusts.

Cons: 1. Uncertainty: With an adjustable-rate mortgage, your interest rate and monthly payments can increase over time, making it harder to plan and budget. 2. Financial risk: If interest rates rise significantly, your monthly payments could become unaffordable. 3. Short-term planning: ARMs are more suitable for those who plan to sell or refinance their home before the initial fixed-rate period expires.

Ultimately, the decision between a fixed-rate mortgage and an adjustable-rate mortgage depends on your personal circumstances and financial goals. Consider factors such as your budget, long-term plans, and risk tolerance when weighing the pros and cons. Consulting with a mortgage professional can also provide valuable insights and guidance to help you navigate the complexities of mortgage rates today.